At least 1.6 billion people worldwide live in substandard housing – but for low-income families in the developing world, the options for financial support to improve their homes are extremely limited.

These households typically have undocumented and volatile incomes and usually lack the collateral needed for a mortgage. Many work in the informal sector and build their homes incrementally as their finances allow. Without access to traditional financial products and services (such as bank accounts and mortgages), it can take these families up to 30 years to complete their homes, with significant impacts on building quality and resilience.

Microfinance institutions (MFIs) offer small loans to people on very low incomes without the need for collateral, typically to start or expand a small business. Globally, MFIs serve an estimated 200 million people, but they officially allocate less than 2% of their funds to housing. Despite this, it is estimated that 10-20% of the loans borrowed for microenterprises are diverted for housing purposes.

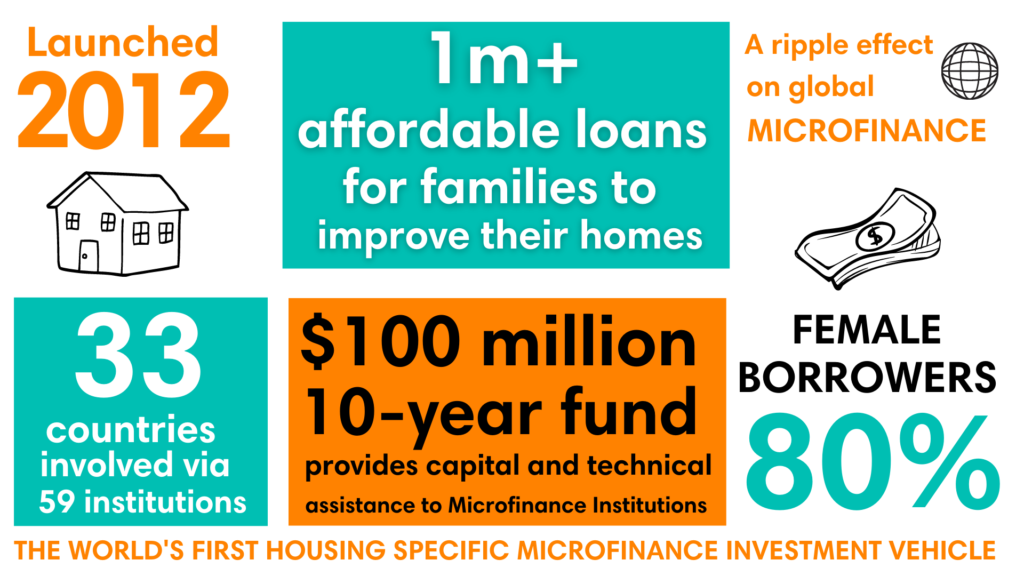

In 2012, Habitat for Humanity launched the world’s first housing-specific microfinance investment fund with the aim of increasing access to loans for housing-related needs in low-income communities. The MicroBuild Fund aims to demonstrate the viability of housing microfinance as an area for investment and to prove its efficacy in addressing the vast global housing deficit.

The $100 million USD fund supplies investment capital to MFI partners across the world and provides customised technical assistance to support them in the development of housing-specific loan products that are tailored to the needs of their clients. The fund has so far helped more than 1 million people access improved housing.

The project in practice

The MicroBuild Fund is managed by the Terwilliger Center for Innovation in Shelter, a unit of Habitat for Humanity International. Triple Jump, Omidyar Network and MetLife Foundation serve as partners and co-owners of the fund.

It was established as a 10-year closed-end demonstration fund with the goal of encouraging the financial sector serving low-income populations to include housing products in their services. It also aimed to prove that social investment funds can yield positive returns for investors, encouraging new and larger institutions to invest in the sector.

Before a partnership is approved, all investee institutions must uphold the industry’s internationally-recognized Client Protection Principles which stipulate that their financial services will be inclusive and delivered transparently. The project recognises that housing is critical to women’s financial empowerment and the Fund encourages that gender considered in the design and delivery of products.

To complement the financial aspect of the loans, MicroBuild helps the institution design housing support services that share knowledge with clients on safe, energy-efficient and resilient construction practices. This support aims to increase clients’ capacity to invest loans wisely, by making more informed decisions around labour, materials and the processes involved in improving their homes.

As of December 2021, MicroBuild has disbursed $151.6 million USD to 59 institutions in 33 countries. The project operates on a truly global scale with a strong presence in Latin America and the Caribbean, which accounts for 42% of allocations, and 21% for Eastern Europe and the Caucasus. Asia accounts for 17% of allocations, while Central Asia, the Middle East and North Africa, and Africa account for 10% each.

The Fund has supported the development of four main home loan product types:

- Home improvement (40.6% of loans)

- Small construction loans (38.6%)

- Formal housing or micro mortgages (14.5%)

- Establishing land tenure or land purchasing (6.3%)

Product innovations include longer-tenure loans. Typical microfinance loans cover a six to 12-month term, however this is not suitable for housing loan products. To facilitate the adoption of housing microfinance products with 36 to 48-month tenures, MicroBuild offered wholesale loans to the financial institutions for the same extended period.

Activities carried out through these loans include:

- Home improvements and repairs, such as roofing and flooring

- Home extensions, such as adding a bedroom, bathroom, or toilet to the existing unit

- New construction on an existing piece of land

- Purchase of affordable housing units that cost less than $15,000 USD

- Energy efficiency measures, for example adding wall insulation and window upgrading

- Land tenure, such as obtaining a title certificate for the existing land and house

MicroBuild has supported residents to build, improve or purchase 209,744 homes and has served 1,048,720 people – more than double the initial target figure of 459,000. The fund has significant outreach to women and rural areas – 80% of borrowers are women and 71% live in rural areas, where poverty is often high and access to safe housing is challenging.

The fund has renewed $47.1 million USD in housing microfinance loans, implying a total fund turnover of $198.7 million USD – almost twice the original capital investment of $100 million USD.

It has impacted the wider housing sector by unlocking more than $582.9 million USD in additional capital by investee institutions to grow their affordable housing finance portfolios, positively impacting an additional 3.5 million people. The housing portfolios of investee institutions now amount to $1.12 billion USD.

Funding

Habitat for Humanity worked with partners to establish the $100 million USD fund of investment capital. The Development Finance Corporation provided $90 million USD of the debt funding, while the remaining $10 million USD was provided by:

- Habitat for Humanity (51%)

- Omidyar Network, through a programme-related investment (20%)

- Triple Jump (4.5%)

- MetLife Foundation (24.5%)

The operating costs for MicroBuild over the past two years have averaged $4,651,078 USD per year. These costs include management fees, legal and audit expenses, professional expenses, maintenance fees, amortised facility costs and hedging interest swaps.

Impact

The project has made housing and home improvements more accessible and affordable to clients across 33 countries. Housing and land ownership has a direct impact on the financial empowerment of community members – particularly women – and enhances their resilience through long-term asset ownership.

The provision of advisory services has increased people’s ability to make good spending and investment decisions, taking out more reliable loans with lower interest rates rather than borrowing from local money lenders. This has resulted in reported feelings of greater choice and control among clients. In some cases, homeowners have been able to leverage their homes to become microentrepreneurs and generate additional income for their families.

Families have gained tangible improvements in their quality of life by investing in building, maintaining and upgrading their homes. Through physical home improvements people feel an increased sense of security and resilience. In Indonesia, for example, 97% of housing microfinance clients reported an improved sense of safety in their homes, whether in possession of formal land ownership documents or not.

Better housing conditions can also lead to an increase in social status, as well as greater feelings of self-worth and pride, garnering more social inclusion, particularly in urban areas. In Indonesia, 71% of female clients reported increased confidence in themselves and their abilities.

Access to loans has enhanced living conditions have improved family relations; for example, through a greater sense of privacy or the provision better spaces to sleep and study for children.

While the environmental aspect of the project is less developed, it recognises that energy-efficient and climate-resilient housing are equity issues. MicroBuild has therefore assisted MFI partners in the design of housing loan products tailored to address energy conservation and structural resilience.

Transfer and expansion

MicroBuild’s transferability is already evident in its global scale. Beyond its direct impact, the project has had significant success in triggering a ripple effect of housing microfinance growth, with the number of MFIs offering housing-specific loans increasing dramatically since 2012.

A key aim of the project is to influence institutions that can unlock additional capital for the affordable housing sector with multilateral agencies and investment banks beginning to bring housing microfinance into their portfolios. Habitat for Humanity’s new partnership with the Asian Development Bank will deliver housing loans to vulnerable and climate change exposed communities in rural and peri-urban areas of Bangladesh, India, Indonesia and the Philippines. This collaboration will help MFIs obtain financing from commercial banks of up to $30 million USD in the first phase.

In March 2020, MicroBuild garnered its first investment in Tunisia through a $60 million USD syndication led by FMO, the Dutch entrepreneurial development bank, further demonstrating its transferability and scalability.

MicroBuild is a closed-end fund and began winding down in July 2019. Access to long-term capital products and services remains a key priority for Habitat for Humanity, however, and the Terwilliger Center has commissioned a feasibility study for a follow-on fund. The second fund will have a stronger climate agenda and will explore new partnerships across the affordable housing value chain, such as local developers and Small and Medium Enterprises (SMEs).

In the 10 years since its launch, MicroBuild has demonstrated the ability of housing microfinance to tackle the challenges faced by more than 1.6 billion people who currently live in substandard housing. Exceeding its own initial target figures, it has designed an adaptable business product that can operate in complex and diverse markets all over the world and has so far served 1 million households that would otherwise not have had access to formal financial services or support.

Goran is 45 years old and an entrepreneur, who provides freelance services repairing and sharpening industrial saws and blades. His wife Larisa (44) works in a health food store as a clerk. They have two children, and both are students; the daughter (21) studies medicine, and the son (19) studies of economics. They live in the suburbs of Sarajevo. They bought the land where their house currently sits in 2010, and have incrementally build and improved their house since 2015. It is still not finished. Their home is 530 sqm with three floors. The ground floor (180sqm) has an open floorplan and serves as Goran’s workspace and office. The second floor, where the family lives, is fully finished and equipped. The third floor is unfinished and used for storage. Larisa and Goran have been Sunrise microfinance clients for many years, taking out both business and housing loans. Last housing loan of 10K BAM (US$5,000) they invested in the facade and thermal insulation.

Goran is 45 years old and an entrepreneur, who provides freelance services repairing and sharpening industrial saws and blades. His wife Larisa (44) works in a health food store as a clerk. They have two children, and both are students; the daughter (21) studies medicine, and the son (19) studies of economics. They live in the suburbs of Sarajevo. They bought the land where their house currently sits in 2010, and have incrementally build and improved their house since 2015. It is still not finished. Their home is 530 sqm with three floors. The ground floor (180sqm) has an open floorplan and serves as Goran’s workspace and office. The second floor, where the family lives, is fully finished and equipped. The third floor is unfinished and used for storage. Larisa and Goran have been Sunrise microfinance clients for many years, taking out both business and housing loans. Last housing loan of 10K BAM (US$5,000) they invested in the facade and thermal insulation.